Table of Contents

Context: Jana Small Finance Bank Ltd has submitted an application to the Reserve Bank of India (RBI) seeking approval for a voluntary transition from a small finance bank to a universal bank.

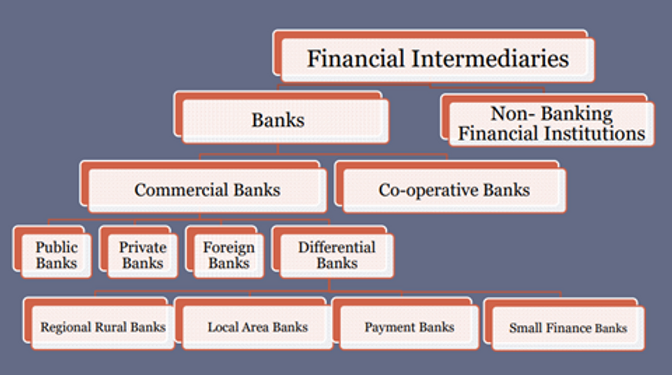

About Small Finance Banks (SFBs)

- Small Finance Banks (SFBs) are financial institutions sanctioned by the RBI, dedicated to offering financial services to low-income individuals and neglected communities, such as microfinance and small-scale banking solutions.

- Scheduled Bank Status: After a period of successful operation, SFBs achieved the status of ‘scheduled banks’ under Section 42 of the RBI Act, 1934.

- Goals of SFBs: The core objective is to facilitate financial inclusion for sections typically excluded from the conventional banking system.

- SFBs strive to provide marginalised populations access to essential financial services, including minor credit facilities, savings, and insurance.

Key Objectives

- Financial Inclusion: Extend banking services to rural and semi-urban areas.

- Microfinance Expansion: Provide affordable credit and banking services to lower-income groups.

- Credit Accessibility: Enhance credit availability for small enterprises, marginal farmers, and micro-entrepreneurs.

Regulatory Framework

- Established based on recommendations of the Nachiket Mor Committee (2014).

- Licensed and regulated by the Reserve Bank of India (RBI) under differentiated banking licenses.

Eligibility and Operational Criteria

- Minimum paid-up equity capital: ₹200 crore.

- Must allocate 75% of Adjusted Net Bank Credit (ANBC) to priority sector lending.

- At least 50% of the loan portfolio must be loans and advances up to ₹25 lakh.

- Mandatory to open at least 25% of branches in unbanked rural areas.

Permitted Activities

- Accept deposits (savings, current, fixed deposits).

- Provide small-ticket loans, primarily microfinance and MSME loans.

- Issue debit and ATM cards.

- Distribution of financial products (insurance, mutual funds, pension) after RBI approval.

Prohibited Activities

- Cannot engage directly in large-scale corporate lending.

- Not permitted to set up subsidiaries for non-banking financial services.

- No foreign operations are allowed.

| Facts |

|

Qualifying Criteria for SFBs

- Indian nationals or professionals residing in India with a minimum of 10 years in senior banking and finance roles.

- Private sector entities, both companies and societies, which are resident-owned with at least five years of successful business operations.

- Pre-existing NBFCs, MFIs, and LABs that are resident-controlled with a track record of five years may transform into SFBs upon meeting all regulatory prerequisites.

Operational Guidelines for SFBs

- Capital Adequacy: A mandatory CRAR (Capital to Risk Weighted Assets Ratio) of 15% must be maintained.

- Priority Sector Commitments: A minimum of 75% of their Adjusted Net Bank Credit has to be allocated to Priority Sector Lending.

- Rural Outreach: At least a quarter of their branches must be situated in previously unbanked rural locales.

- Capital Requirements: SFBs must possess a minimum paid-up voting equity capital of Rs. 200 crore.

- Regulatory Framework: SFBs operate as public limited companies under the Companies Act, 2013, and are regulated by the Banking Regulations Act, 1949; the RBI Act, 1934; and directives issued from time to time.

Key Features of Small Finance Banks (SFBs)

- Purpose: SFBs aim to provide basic banking services and credit facilities to segments traditionally excluded from formal banking channels.

- Regulation: Governed by RBI regulations, SFBs adhere to prudential norms and regulations applicable to commercial banks, ensuring financial stability and accountability.

- Priority Sector Lending: SFBs are mandated to allocate a significant portion (75%) of their total net credit to priority sector lending, supporting sectors such as agriculture, MSMEs, and low-income households.

- Loan Portfolio Composition: A substantial portion (50%) of SFBs’ loan portfolio must consist of advances up to Rs 25 lakh, facilitating access to credit for small borrowers and entrepreneurs.

- Branch Network Expansion: SFBs are required to establish branches in unbanked and underbanked areas, particularly in rural and semi-urban regions. Initially, at least 25% of branches must be located in unbanked rural areas, enhancing financial access.

Capital Requirement and Regulation

- Minimum Capital: SFBs must have a minimum paid-up voting equity capital of Rs. 200 crore, except for those converted from UCBs.

- Legal Status: Registered as a public limited company under the Companies Act 2013 and licensed under section 22 of the Banking Regulation Act, 1949.

- Regulatory Framework: Governed primarily by the Banking Regulation Act, 1949, the RBI Act, 1934, and other relevant statutes, SFBs operate within a robust regulatory framework to ensure transparency and accountability.

Comparison of Small Finance Banks (SFBs) and Universal Banks

|

Comparison of Small Finance Banks (SFBs) and Universal Banks |

||

| Aspect | Small Finance Banks (SFBs) | Universal Banks |

| Scope of Activities | Primarily cater to underserved segments like small businesses, farmers, MSMEs. | Offer a wide range of services to all customer segments, including corporate and retail banking, investments, forex, etc. |

| Minimum Capital Requirement | ₹200 crore | ₹500 crore |

| Credit Requirements | Minimum 75% of Adjusted Net Bank Credit to priority sectors | 40% of Net Bank Credit to priority sectors |

| Focus Segment | Unbanked, semi-urban, rural, micro-enterprises | All customer segments (retail, corporate, etc.) |

| Branch Expansion | Mandatory 25% of branches in rural/unbanked areas | No mandatory specific ratio, but have rural presence norms |

| Foreign Operations | Not permitted | Allowed |

| Regulatory Framework | Regulated under RBI’s differentiated banking norms | Regulated under RBI’s universal banking norms |

| Deposits and Lending | Accept deposits; focus on small-ticket lending | Accept deposits; diverse lending and financial services |

| Investment Activities | Limited involvement | Wide-ranging investment banking and market operations |

Small Finance Banks play a vital role in advancing financial inclusion and socio-economic development in India. Through their focus on priority sector lending, inclusive branch network expansion, and adherence to regulatory norms, SFBs contribute significantly to the country’s inclusive growth agenda. As drivers of financial empowerment and inclusion, SFBs continue to evolve, leveraging innovation and technology to reach underserved communities and foster economic resilience.

Oor Pare Prehistoric Site: Location, Roc...

Oor Pare Prehistoric Site: Location, Roc...

Assam Election 2026: Exit Poll, Result D...

Assam Election 2026: Exit Poll, Result D...

Great Indian Bustard (GIB): Features, Th...

Great Indian Bustard (GIB): Features, Th...