Table of Contents

Context: NITI Aayog released the second edition of the joint report From Borrowers to Builders, highlighting that women now hold a ₹76 lakh crore credit portfolio, accounting for 26% of India’s total system credit.

Factsheet of Report on From Borrowers to Builders

- Massive Portfolio Growth: Women’s outstanding credit grew 8x from ₹16 lakh crore in 2017 to ₹76 lakh crore in 2025.

- Rising Penetration: Credit penetration among women nearly doubled, rising from 19% in 2017 to 36% in 2025.

- Commercial Credit Surge: Business-purpose loans for women grew at a 31% CAGR over the last three years, significantly outperforming the overall commercial credit growth of 17%.

- Efficiency Gains: Same-day loan approvals for women in consumption categories increased from 34% in 2022 to 45% in 2025, driven by digital onboarding.

Current Status of Credit for Women

- Shift to Secured Assets: Women are increasingly participating in long-term asset ownership, with their share in housing loan originations rising to 69% in 2025.

- Microfinance Graduation: Approximately 19% of active microfinance borrowers have successfully graduated to individual retail or commercial loans.

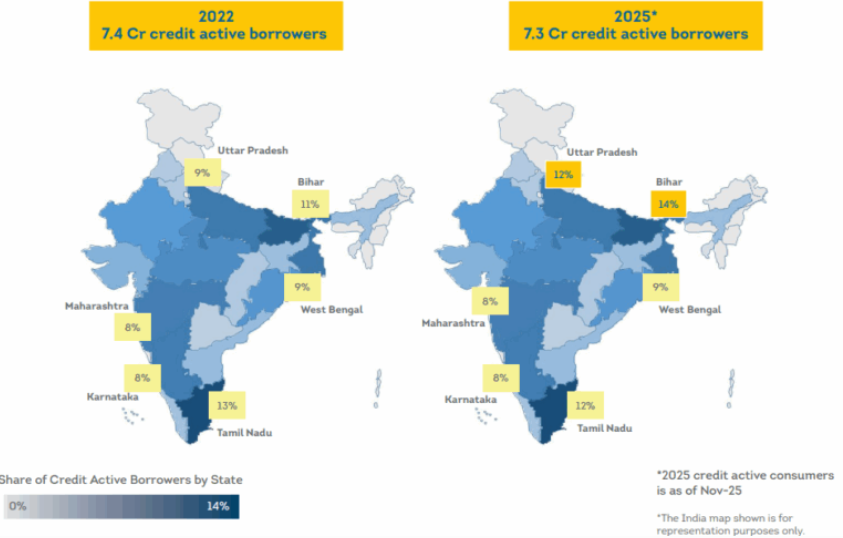

- Geographic Expansion: While southern states like Tamil Nadu lead in volume, northern states like Bihar (59% CAGR) and Uttar Pradesh (42% CAGR) are seeing the fastest growth in women business borrowers.

- Younger Cohort Participation: Women under 35 are accelerating credit uptake across gold, consumption, and vehicle loans, with 1 in 3 young housing loan borrowers being women.

- Responsible Borrowing: Women maintain resilient credit profiles, with a default rate 0.7x lower than overall credit originations as of 2024.

Challenges Associated with Women’s Credit

- Untapped Potential: Nearly two-thirds of credit-eligible women (approx. 29 crore) remain unserved by formal financial systems.

- Decision-Making Gaps: Many rural women nano-entrepreneurs (RWNEs) lack full autonomy over credit and investment decisions, limiting the strategic use of borrowed funds.

- Digital Translation Gap: While smartphone use is high, many women struggle to understand how AI or advanced digital tools can directly improve their business marketing or planning.

- Time Poverty: Overlapping household responsibilities and unpaid care work (cited by 38% in Kerala) limit women’s ability to engage consistently with digital credit platforms.

- Structural Barriers: Nano-enterprises often lack formal collateral, making them reliant on entry-level products and vulnerable to credit supply contractions.

Initiatives Taken by the Government

- Digital Public Infrastructure (DPI): Aadhaar e-KYC, UPI, and DigiLocker have lowered entry barriers for first-time women borrowers in rural areas.

- Women Entrepreneurship Platform (WEP): A NITI Aayog initiative that aligns financial institutions and CSOs to support women in moving from initial access to sustained growth.

- Financing Women Collaborative (FWC): Launched in 2023 to bridge sex-disaggregated data gaps and coordinate the financing ecosystem for women entrepreneurs.

- Project Seher: A TransUnion CIBIL credit education program aimed at strengthening credit literacy and awareness among women.

- Government Incentives: Interventions like specific stamp duty benefits have actively encouraged women to take up housing loans.

Way Ahead

- Flow-Based Underwriting: Integrate digital footprints (UPI trails, merchant activity) as productive economic assets to assess creditworthiness for collateral-free nano-enterprises.

- Lifecycle-Based Products: Develop gender-intelligent bundles that integrate savings, credit, and insurance specifically for younger women under 35.

- From Access to Progression: Shift policy focus from just disbursement volumes to tracking graduation rates and multi-product holdings to ensure enterprise maturity.

- Trust-Based Capability Building: Leverage social networks and collectives (SHGs/Federations) to provide peer-endorsed digital training that builds long-term confidence.

- Inclusive Design: Financial tools must be vernacular-first and voice-enabled to accommodate diverse literacy levels and contextual constraints.

Regulatory Issues in India’s Nuclear P...

Regulatory Issues in India’s Nuclear P...

Deep-Space Distance Measurement: New Tec...

Deep-Space Distance Measurement: New Tec...

Elephanta Island Excavations: New Discov...

Elephanta Island Excavations: New Discov...